Public Private Partnerships: infrastructure financing and structuring cash flows

Training ByteSize, in conjunction with Maurice Diamond, have produced a series of short presentations which focus on specific areas of APMG’s CP3P certification.

In this second blog and video we look at infrastructure financing and structuring cash flows. This is often an area of Public Private Partnerships that students find difficult to understand, so this will benefit anyone going on a CP3P course or studying for their CP3P certification exam.

If you would like to download this presentation as a PDF click here.

Infrastructure Financing and Structuring Cash Flows

What we know about Public Private Partnerships

Hi, my name is Martyn Kinch, I’m Chairman at Training ByteSize. Together with Maurice Diamond, our lead Public Private Partnership (PPP) and CP3P trainer, we have put together a number of short videos around public private partnerships, which I hope you’ll find useful .

Maurice Diamond is a Fellow of the Chartered Institute of Public Finance and Accountancy with extensive UK and international PFI and PPP experience. He has been involved in PPP in its various guises since its inception.

Maurice has advised on PPPs in the UK, Europe, Africa, and Asia for over 20 years and provided coaching, awareness, education and training on PFM (public financial management) and PPP (public private partnerships) for senior civil servants, government ministers, PPP practitioners and the private sector. He is also an accredited CP3P Foundation trainer.

Training ByteSize has been delivering PPP and CP3P training for many years now across the world and have one of the most experienced training teams available. The CP3P certification program aims to foster a common minimum level of knowledge and understanding amongst individuals working on PPPs or those interests in learning about PPPs, regardless of discipline or sector.

About the CP3P certification

The certification has been designed to create a consistency of terms using Public Private Partnerships and as a process for delivery of PPP projects worldwide. The term PPP stands for Public Private Partnerships and is both used and misused in equal measure. PPP is a useful way for the public sector to renew and develop its infrastructure and economy.

However, there are still many procurement practitioners who do not understand the key differences, to understand a procurement and a PPP. Sometimes this can be the primary cause of PPP procurement failure, either because a feasibility study is flawed and, or the deal has been poorly prepared and presented, and it therefore attract bidders and investors, or it fails to deliver improved value to the taxpayer.

A PPP Practitioner not only needs to understand project management, but prior and effective and realistic business cases, undertaking fair, competitive, and transparent procurement and contract management. They also need to understand the key tenants of PPP.

There also many people in the public sector who are not familiar with some of the key features of a PPP, the CP3P qualification, which is sponsored by the world bank and its agencies and accredited by the APMG seeks to overcome this problem.

This series of short talks focuses on these areas of the APMG syllabus that make a difference, and in this second session we focus on infrastructure financing and structuring cash flows.

Infrastructure financing and public sector outflows

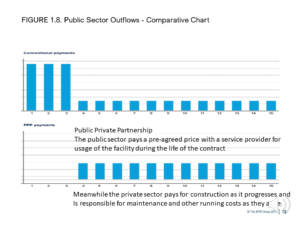

So first of all, let’s look at figure 1.8 drawn from the CP3P guide produced by APMG. This is the public sector outflows, and it’s a comparative chart between a conventional procurement and a Public Private Partnership.

Now under a conventional procurement or traditional procurement, the government pays for construction as it progresses, and then is responsible for maintenance and other running costs as they arise.

Under a Public Private Partnership, the public sector pays a pre-agreed price with a service provider for usage of the facility during the life of the contract, and only when the services commence. Meanwhile, the private sector pays for construction as it progresses and is responsible for

maintenance and other running costs as they arise.

So we can see here that the amount that the public sector is paying during that period of service operations is slightly higher than it would be under a conventional procurement. But then on the other hand, the public sector has not made any upfront capital payments. And indeed the quality of that service delivery is what will cause the private sector to be paid.

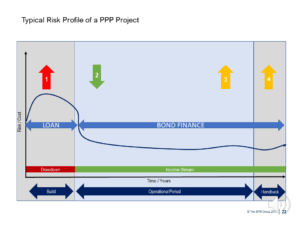

Risk profile

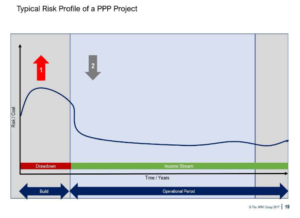

Now, let’s look at the risk profile of one of these deals.

Now, let’s look at the risk profile of one of these deals.

So here, we’re going to show the risk over time for a typical Public Private Partnership. So we’ve got risk costs up on the left-hand side, running across the bottom is time or years now. There are effectively two periods for a PPP; one of them is the build phase and that’s followed by the

operational phase.

However, towards the end of the operational phase, we have a period which is prior to a hundred back before the asset is returned to the public sector. During that period, the private sector SPV, may have to put money into maintaining some of the assets such as a roof and so on. So that becomes a more risky period.

Let’s continue to look at the risk profile of a typical Public Private Partnership.

Let’s continue to look at the risk profile of a typical Public Private Partnership.

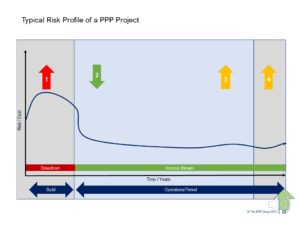

Here we have the line which is a perceived level of risk in the deal at any point in time, and that is shown as being very high during the first period during that construction period. That’s the period during which the SPV will be drawing down its loan from the bank in order to pay it’s a building contract.

Then we move into the operational period when the risk falls dramatically, this is the green number two arrow.

Although initially there might be some additional level of risk associated with setting up the services, setting up the systems associated with the delivery of the contract.

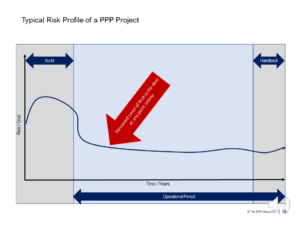

As we move towards the end of the contract period to arrow number three, let’s say this was a 25 to 30 year deal. We might be in that period between the 15 and 22, where there’ll be a bit of a hump in risk, because we might see that some of our infrastructure might not be operating effectively and

As we move towards the end of the contract period to arrow number three, let’s say this was a 25 to 30 year deal. We might be in that period between the 15 and 22, where there’ll be a bit of a hump in risk, because we might see that some of our infrastructure might not be operating effectively and

might need to be replaced. Of course we will have set aside a maintenance fund as we were going through the each year of the contract to pay for any issues that might arise.

Finally in that handback period which arrow number four indicates, there may be again some additional risk. We know that we’re going to call the independent engineer or independent certifier to look at the asset and they will take a view on whether or not there is sufficient life left in certain

parts of the asset that had been specified in the contract that go beyond contract term, let’s say for three to five years.

If the asset is not sufficiently robust in that way, then the expectation is that the SPV will have to restore let’s say the quality of the roof and to put it in good order, at least say that it is sufficiently robust to loss for the period that has been demanded in the contract at the beginning of the contract, maybe 25 or 30 years earlier.

If the asset is not sufficiently robust in that way, then the expectation is that the SPV will have to restore let’s say the quality of the roof and to put it in good order, at least say that it is sufficiently robust to loss for the period that has been demanded in the contract at the beginning of the contract, maybe 25 or 30 years earlier.

So we have initially the start of our contract where all the risk is ahead of us, those construction, where the risk has dropped considerably. We might now think about refinancing our loan, or perhaps we will have had a three to five year relatively short term loan. And now we are going to be looking at bond finance for the rest of the contract period.

The risk then increases as we move to that mid-life period of the contract. And then ultimately, we get to the end of the contract. Although the risk is maybe increasing, there’s a possibility that the asset is in fully good order and the independent certifiers signed it off and we can simply move to term. In which case, if there is a fund that’s been put together associated with the maintenance around hand back then that fund can be released to the equity shareholders.

So we could either have low, loan finance, that is throughout the whole period of the contract. Although that actually became quite a difficult to obtain, after the financial crisis in 2007, 2008, more likely we’ll see that there will be a loan followed by bond finance as illustrated in the diagram.

Thank you. That brings us to the end of our second seminar in project finance and SPV’s. In the next session we are going to look at the shareholders of the equity shareholders and debt finances in an SPV.

Hi there, we’re Training ByteSize

As experts in delivering accredited project management and IT service management training through a range of study styles, your success is key to our success.

We understand how people learn, we know how to train people to pass exams, we employ the best trainers and specialise in small class sizes to help you get the best from your investment. So, if you’re looking to enhance your project management skills and ensure you pass first time, Training ByteSize is a name you can trust.

We thrive on providing a reliable service to customers and we are proud to maintain an exceptional renewal rate with our corporate clients. Perhaps one of the biggest reasons for this success is our bespoke approach; we provide the training in the exact way you want it, whether that is on-site, online, virtual, classroom based or a combination of these.

As a family-run business we’re small enough to care, but big enough to support clients from start to finish in the way they would like to learn.

Our ability to adapt to the changing environment of learning and training ensures we remain at the forefront of the industry, which is why we continue to be first choice for many blue-chip clients. When you train with us, you’ll know straight away that you’ve made the right choice.

So, when people ask what’s the difference between us and our competitors, its quite simply us.

Study your CP3P certification with us

Achieving the APMG CP3P certification will give you the knowledge and skills to speak the common international language used to deliver PPP’s. Being a formal certification it will also bring international credibility to your career. This qualification will ensure you understand the roles, processes and sequence in which tasks need to be completed in a public-private partnership.

At Training ByteSize, we offer three levels of accreditation for PPP Professionals. Our Certified PPP Professional (CP3P) Level 1 Foundation course will give you an introduction to Public-Private Partnerships and explain the core terminology, processes and systems you’ll need to know.

The Certified PPP Professional (CP3P) Level 2 Preparation Course is provided at an Intermediate level. So, it’s ideal for those who have a basic understanding of Public-Private Partnerships but want to expand on their practical knowledge and application of skills. The course will enable you to demonstrate an understanding of how to apply and tailor the established procedures, roles and institutional responsibilities that determine how the government selects, implements and manages PPP projects, as outlined in the PPP Guide.

Finally, the Certified PPP Professional (CP3P) Level 3 Execution Course is aimed at individuals involved in the structuring and tendering of PPP projects and the management of PPP contracts, mostly public sector officials, practitioners and their advisors or consultants.

To learn more about becoming a certified PPP Professional as well as the variety of course options we provide, you can email our expert team; we are on-hand to talk you through the most suitable course for you and your career aspirations.